The Tax Cuts and Jobs Act from 2017 (“TCJA”) limits state and local tax (SALT) deduction for individuals and trusts to $10,000 for 2018 – 2025 tax years. As a result, many taxpayers receive a limited federal tax benefit from the state taxes they pay, particularly owners of businesses taxed as pass-through entities (S-Corporations and Partnerships).

Importantly, the TCJA did not specifically limit the amount of state taxes business entities can deduct, which includes S-corporations and partnerships. The IRS issued Notice 2020-75 in late 2020 that allows for pass-through entities (“PTE”) to deduct state taxes it pays on behalf of its owners.

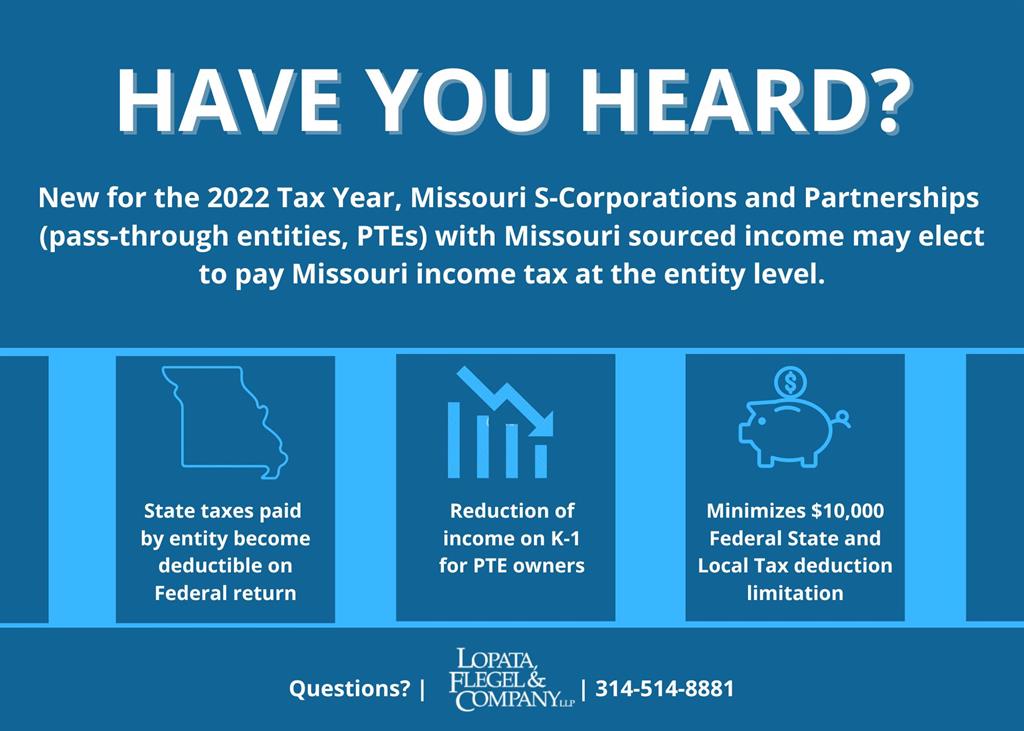

Just this summer, Missouri implemented an optional pass-through entity tax (“PTET”) effective for tax years ending on or after December 31, 2022. The PTET is a new way for entities (S-corporation and Partnerships) to pay state taxes for their owners without being subject to the maximum $10,000 deduction for state taxes on individual or trust income tax returns. This creates some level of parity with taxable corporations that have been allowed to deduct state and local taxes for their federal tax returns.

Since 2018, if an individual pays $50,000 of Missouri income tax on their S-corporation income, their SALT for purpose of itemized deductions includes the Missouri tax on their S-corporation plus their state income taxes on other earnings, real estate and personal property taxes. Their itemized SALT deduction on their individual federal income tax return is limited to $10,000. Using a PTET election, the S-corporation would instead pay the $50,000 of tax, and deduct the full amount of the Missouri tax; thus gaining a significant deduction. This reduction in federal taxable income will save federal taxes depending on the individual’s marginal tax of an amount that could be in excess of 40% of the state tax deduction and effectively lower an individual’s overall tax rate by 1-2%.

Electing into the PTET may generate large federal tax savings, and even more so for taxpayers who don’t itemize deductions. Missouri has not yet provided guidance on when to make the PTET election or how to pay estimated taxes under the PTET election. We will provide updates as guidance is issued. Many other states have passed similar legislation.

If you are an owner of a pass-through entity that is a client of our firm, we will be contacting you in the coming month. If you are an owner or investor in an entity that is not our client, please feel free to contact us to discuss the possible tax savings.

We are very excited about this opportunity to help our clients realize meaningful tax savings. Partners of our firm have been extremely active in helping move Missouri toward allowing the PTET deduction; including submitting a detailed memorandum, meetings with Missouri legislators, and a personal meeting with the Director of the Missouri Department of Revenue.